Insights

Market rebound defies pessimism

Markets have once again confounded the sceptics. Following a period of sharp declines and heightened volatility triggered by US tariff announcements earlier this year, global equities have bounced back—hitting new record highs in record time.

This rapid recovery was fuelled by a combination of softened trade rhetoric by Donald Trump, stronger-than-expected corporate earnings, and resilient investor sentiment. Risk appetite returned quickly, evidenced by a standout performance in US high-beta stocks. The top quintile of riskier equities delivered a remarkable 24% return over the quarter, marking one of the strongest performances on record in that segment.

This rebound marks a significant reversal from the lows seen in early April—once again reinforcing the view that betting against the US expansion remains a risky strategy.

Corporate Profits Hold Up Despite Policy Uncertainty

In the immediate aftermath of the initial tariff announcements, many analysts trimmed profit expectations by around 5-6%, anticipating that some trade measures would be implemented and that companies would respond by adjusting supply chains and pricing strategies.

Since then, however, earnings outlooks have remained largely steady. In the US, confidence has been further buoyed by the passage of the “One Big Beautiful Bill Act”, which is expected to support further upgrades. In particular, the technology sector continues to ride high on the ongoing artificial intelligence investment wave, with Q1 results indicating robust demand and capital spending.

European companies have not enjoyed quite the same tailwinds. A stronger euro is weighing on exporters, and earnings momentum remains more subdued. Even so, many forecasters are forecasting profit growth of around 5% for this year, rising to 12% in 2026 - an outlook that continues to favour equities.

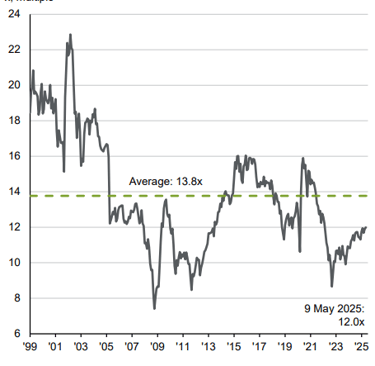

Valuations Elevated, Leaving Less Room for Error

The sharp market recovery has, however, pushed US valuations to stretched levels, increasing the risk of a pullback if policy or macroeconomic concerns resurface—particularly around tariffs. With little room for mis-steps at current prices, investors may want to tread cautiously.

In this environment, “value” opportunities are starting to look compelling. Globally, the valuation spread between the most and least expensive stocks now sits in the 78th percentile, based on data going back 30 years. Markets like the UK are continuing to trade on multiples below their 30-year average (on a PE basis).

“Traditional” sectors like financials and energy look attractive from a valuation perspective, while technology looks expensive to us. Defence names in Europe and Asia, long overlooked, have rallied sharply amid rising geopolitical tensions and a renewed focus on military spending.

European Banks Stage an Unlikely Comeback

Among the more unexpected market stories of recent years is the resurgence of European banks. Once written off by investors, the sector has enjoyed a revival driven by rising interest rates, streamlined cost structures, and robust balance sheets.

Since 2020, many leading European banks have seen their share prices triple. In the first half of 2025 alone, the sector posted a 45% gain in US dollar terms—outpacing many high-profile US technology names.

While earnings momentum remains healthy and credit risks appear contained, there are signs of caution emerging. Increased merger activity—some of it questionable in terms of strategic value—could erode shareholder returns. Even so, the recovery underscores the potential in traditional, undervalued sectors with improving fundamentals.

Reform Gathers Pace in Asia

Asia is also seeing a significant shift, as corporate governance reforms begin to reshape investment narratives. Japan has led the way, with pressure mounting on firms to prioritise shareholder returns. Buybacks and dividend hikes have steadily accelerated in recent years.

Other markets are following suit. China has recently seen its net share issuance turn negative for the first time, as firms favour repurchases over expansionary capital spending. Meanwhile, South Korea has launched a formal “value up” initiative, aimed at unlocking hidden value among its large, often opaque conglomerates.

Investors have responded with enthusiasm—perhaps too much so in the near-term. Korean equities had surged over 40% year-to-date (USD terms) by the end of Q2. While the policy direction is welcome, meaningful change will take time, and valuations now look stretched to us.

Nonetheless, the broader trend is clear. As firms across Asia improve capital discipline and focus on shareholder value, long-term returns should improve, potentially narrowing the gap with US markets after more than a decade of US outperformance.

Cautious Path Forward for Investors

While the optimism in markets is justified by resilient profits and ongoing reform, risks remain. Policy uncertainty, particularly around trade and tariffs, could quickly re-enter the spotlight. With equity valuations high and expectations elevated, any surprises could have an outsized impact.

However, the global investment landscape is evolving. Traditional value sectors—from European banks to Asian industrials—are showing new signs of life. ESG concerns, capital efficiency and shareholder returns are becoming increasingly central to investment decisions.

For investors willing to look beyond the obvious winners, opportunities still exist—particularly among undervalued firms with improving fundamentals.

In this environment, whilst cautiously optimistic, our portfolio biases are towards the value-orientated UK market. Our US exposure is largely via a “buffer” fund, which participates in most (but not all) of the market’s upside, whilst offering downside protection.

1st August 2025

Gary Waite

Portfolio Manager

_________________________________________________

UK FTSE All Share forward P/E ratio

X, multiple